AI's $250B Answer: Beyond Cahn's Revenue Focus, Google's Cost-Cutting Potential and AI ROIC Growth

David Cahn’s 'AI’s $600B Question' has sparked discussions across the tech world about AI’s potential to drive top-line growth, but I’m here to argue that the real value may lie in cost savings.

On June 20, 2024, David Cahn from Sequoia published "AI's $600B Question." In the article, Cahn examines NVIDIA’s projected Q4 2024 data center segment revenue run rate of $150 billion, estimating it to support a global AI revenue potential of $600 billion, justifying significant CapEx investments worldwide.

While Cahn’s view that AI must drive substantial top-line growth for companies to achieve ROI has merit, I believe it overlooks AI’s potential as a powerful cost-cutting tool. For instance, in Google’s recent Q3 earnings call, they revealed:

“Today, more than 1/4 of all new code at Google is generated by AI, then reviewed and accepted by engineers. This helps our engineers do more and move faster”

This is an extraordinary development. AI’s role in automating code generation is already transforming software engineering at Google. In this post I will:

perform a quick case study on potential value creation and margin expansion by Google’s AI tools

illustrate how AI has already made a substantial impact on ROIC and sales growth at many of the hyperscalers.

1. AI’s potential as a cost-cutter

A Glimpse Into the Future…

While AI may not yet be advanced enough to fully replace software engineers, the rapid progress in large language models suggests we're approaching that possibility. Startups like Cognition Labs, creator of the coding assistant Devin AI, are already valued at over $2 billion, underscoring the high expectations and potential in this space. It’s clear that the world is edging closer to the creation of a fully autonomous AI software engineer—and Google may be closer to achieving this than we realize.

Additionally, looking at Google’s cost structure over time, Google has cut its SG&A costs 10% since 2020 while largely not cutting R&D expenses at all.

I believe that Google’s in-house AI products have the power to create tons of value. Google revealed this power itself when the company revealed how much of the code contained in Google products is literally generated by AI.

I decided to model potential cost savings if Google were to reduce software engineering expenses through AI. Using Google’s current R&D cost run rate, I estimated the following savings scenarios.

If Google could cut 25% of its software engineering workforce, it would save around $12.45 billion annually. With a typical software engineer at Google earning $450,000, this equates to over 25,000 potential roles reduced via AI. Compared to Google’s estimated $52 billion CapEx on AI-related products, these cost reductions could yield substantial returns.

This makes even more sense when thinking about the value brought to the business by these cost cuts. Google trades at around 20x its operating income (EBIT), so the implied value created by these cost cuts alone could be monstrous.

The cost cuts calculated don’t even begin to tap into Google’s SG&A expenses (which make up more than 26% of its revenue). Can you imagine the savings Gemini has the ability to replace the jobs of employees in finance, human resources, information technology, and other areas?

So What Just Happened?

We just concluded that Google’s ability to cut R&D costs using AI in the future may be able to bring almost $250B of value to the business, solely from R&D cost-cutting alone. While it’s easier said than done to cut R&D costs by 25%, it still is useful to perform this What-If analysis as the impact of AI will cause many substantial operational improvements among public companies. So while Cahn may have a point about the top-line necessity of AI, it’s essential to consider AI’s impact within organizations from an operational standpoint.

2. AI CapEx Has Already Started to See ROI

AI Businesses are still Generating Significant Revenue

While the first part of this article focused on AI’s ability to cost-cut, that shouldn’t diminish from the fact that AI products still grow the top-line as Cahn first mentioned. Consider a select few quotes from recent earnings calls.

Google: “Gemini API calls have grown nearly 14x in a 6-month period.” -

Amazon: “AWS's AI business is a multibillion-dollar revenue run rate business that continues to grow at a triple-digit year-over-year percentage and is growing more than 3x faster at this stage of its evolution as AWS itself grew”

Microsoft: “We're excited that only 2.5 years in, our AI business is on track to surpass $10 billion of annual revenue run rate in Q2. This will be the fastest business in our history to reach this milestone.”

Meta: “Meta AI now has more than 500 million monthly actives.”

The Impact of these Statements

Consider a company like Microsoft that currently trades at 12.4x sales, $10B in AI product revenue results in $120.4B in value created for the business. How impressiv is that for a return on CapEx?

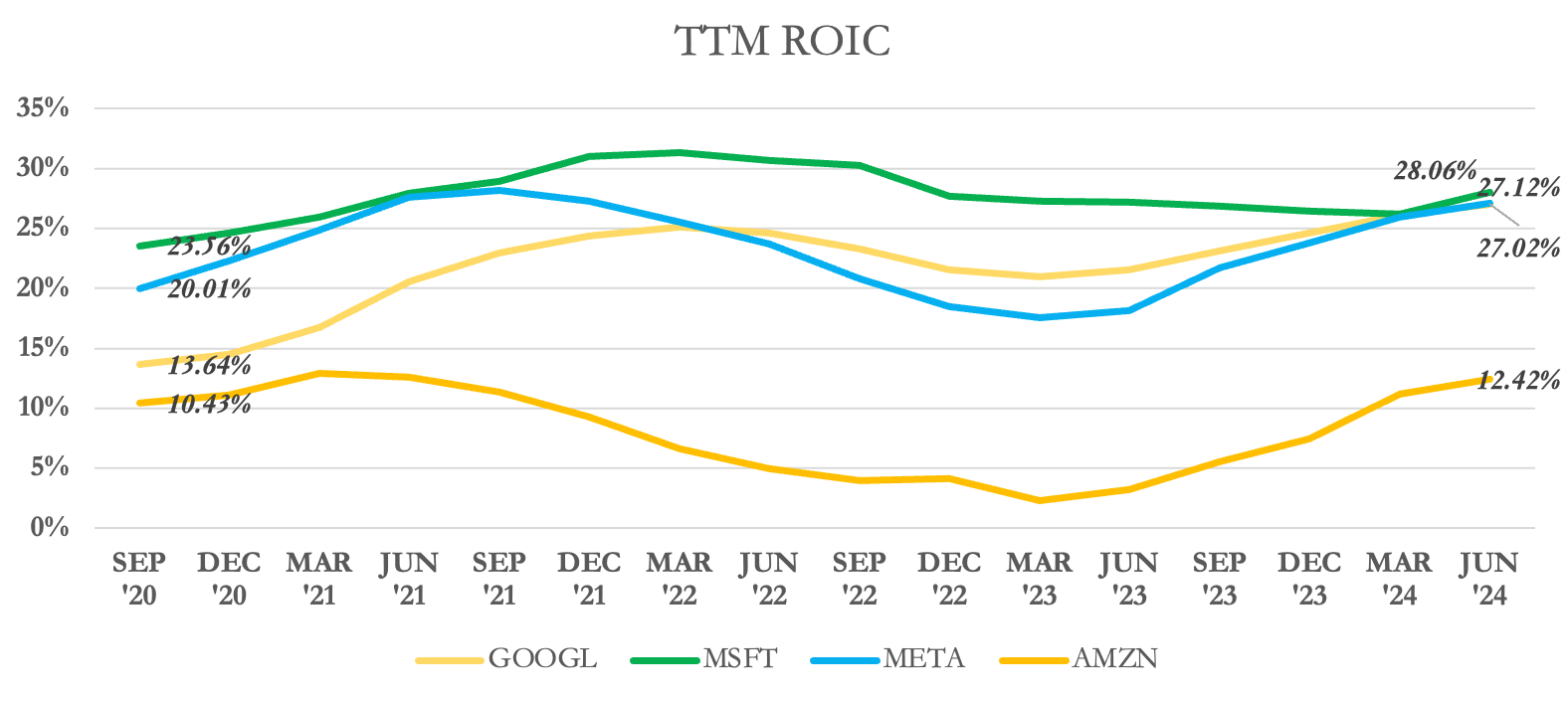

Growing ROIC for Hyperscalers

Finally, I want to end this writeup with an analysis of a metric that I have written about before, one called return on invested capital (ROIC). ROIC measures how effectively a company uses its capital to generate profits. It is calculated by dividing a company's net operating profit after taxes (NOPAT) by its invested capital. Ever since hyperscalers began ramping up AI CapEx, ROIC has increased by an average of 6.5% at each one of the hyperscalers. This growth alone may justify AI CapEx. Logically if Microsoft can spends its cash to generate 28% returns while simultaneously improving its core business, that’s a pretty good deal.

Finally, consider a quote from Gavin Baker (star of my last post) as he appeared on the Invest Like The Best Podcast. It will jog your brain regarding AI’s potential.

“There has been a massive ROI on AI. What are we talking about?… There is something called return on invested capital, and ROIC has gone up for all of these companies since they ramped CapEx. What are we talking about?

If you're an AI ROI skeptic, why has ROIC got up at these companies? Well, yes, CapEx is up. NOPAT is up more. Why is that? Because they're doing exactly what you would expect to happen in a world of AI, they're trading off human labor against GPU hours. That's why the ROIC has gone up and the GPUs are really efficient. Let's have an AI ROI debate when the ROIC at the big AI spenders starts to go down.”

In Summary: AI as a Dual Force for Cost-Cutting and Growth

In sum, AI’s impact extends beyond just top-line growth. It’s also a transformational cost-cutting tool that can drive value internally for companies. As Google demonstrates, AI’s ability to reduce R&D costs alone may add up to $250 billion in long-term value. While it may not be simple to achieve a 25% reduction in R&D costs, this “What-If” analysis emphasizes AI’s potential to revolutionize operations.

Ultimately, while David Cahn’s perspective on the top-line necessity of AI is valid, it’s essential to recognize what we’re subtracting by when calculating Revenue - Expenses = Profit. As companies like Google and Microsoft continue to harness AI’s potential, they are proving that AI is not just a growth driver—it’s an asset that reshapes core business operations, delivering returns on CapEx from both revenue growth and cost efficiencies.